Subject to the provisions of paragraph 2 of article 18, pensions and other similar remuneration, including social security payments, beneficially owned by a resident of a contracting state shall be taxable only in that contracting state. While japan ratified the protocol in the diet on june 17, 2013, ratification on the us side had been held up in the senate, which finally ratified it on july 17, 2019.

Pdf Meaning Of Permanent Establishment In Article 5 Of Double Tax Conventions

Security taxes to both the united states and japan for the same work.

Us japan tax treaty article 17. Entry into effect (a) the provisions of the mli shall have effect in each contracting jurisdiction with respect to the tax treaty between japan and the united arab emirates: Japan is a member of the united nations (un), oecd, and g7. The convention between the government of the united states of america and the government of japan for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income and the protocol, which forms an integral part of the convention, signed at washington on november 6, 2003

Notable changes in the protocol are enlarged exemptions of taxes required to be withheld on. Notwithstanding the provisions of articles 14 and 15, income derived by an entertainer, such as a theatre, motion picture, radio or television artiste, and a musician, or by an athlete, from his personal activities as such may be taxed in the contracting state in which these activities of the entertainer or athlete are exercised. Although the protocol was signed on 25 january 2013 and approved by the japanese diet on 17 june 2013, it took 6 years and 7 months from the signature to the enactment due to additional time necessary for us ratification procedures.

(a) where a resident of japan derives income from the united states which may be taxed in the united states in accordance with the provisions of this convention, the amount of the united states tax payable in respect of that income shall be allowed as a credit against the japanese tax imposed on that resident. (b) has a substantial presence, permanent home or habitual abode in the united states; Japan has concluded 65 tax treaties which apply to 96 jurisdictions (shown in the annex).

The protocol was originally signed by japan and the us on january 24, 2013. Although the protocol was signed on 25 january 2013 (japan time) and approved by the japanese diet on 17 june 2013, A convention between the united states and japan for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income was signed at tokyo on march 8, 1971.

Citizen or an alien lawfully admitted for permanent residence in the united states under the laws of the united states shall be regarded as a resident of the united states only if the individual: • foreign treaties ‘taxes covered’ vary from treaty to treaty The president signed it into law on august 6, 2019.

Convention between the united states of america and japan for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income, signed at tokyo on march 8,1971. Subject to the laws of japan regarding the allowance as a credit against japanese tax of tax payable in any country other than japan: Attachment for limitation on benefits article.

The provisions of paragraph 4 shall not affect the benefits conferred by a contracting state under paragraphs 2 and 3 of article 9, paragraph 3 of article 17, and articles 18, 19, 23, 24, 25 and 28, but in the case of benefits conferred by the united states under articles 18 and 19 only if the individuals claiming the benefits are neither citizens of, nor have been lawfully admitted for permanent residence in, the. Klaster kemudahan berusaha bidang perpajakan; (a) is not a resident of japan under paragraph 1;

The following paragraph 1 of article 17 of the mli applies and supersedes the provision of this agreement: A taxpayer wishing to claim treaty benefits is required to go through certain procedures provided for in the law concerning special measures to the Under the agreement, if you work as an employee in the united states, you normally will be covered by the united states, and you and your employer will pay social security taxes only to the united states.

Article 7 of the mli —. Ratification between the government of japan and the government of the united states of america. Japan tax bulletin procedures for claiming tax treaty benefits april 2016 4.

The protocol was originally signed by the us and japan on january 24, 2013. Ratification was advised by the senate of the united states on november 29, 1971. Article 17 pension in the us tax treaty with japan.

The otherwise delectable article 17 is rendered impotent by article 1(4)(a), which states that, subject to a few minor exceptions (in which article 17(1) is not included), “… nothing in the treaty has any affect on the taxation by the u.s. If you work as an employee in japan, you normally will be

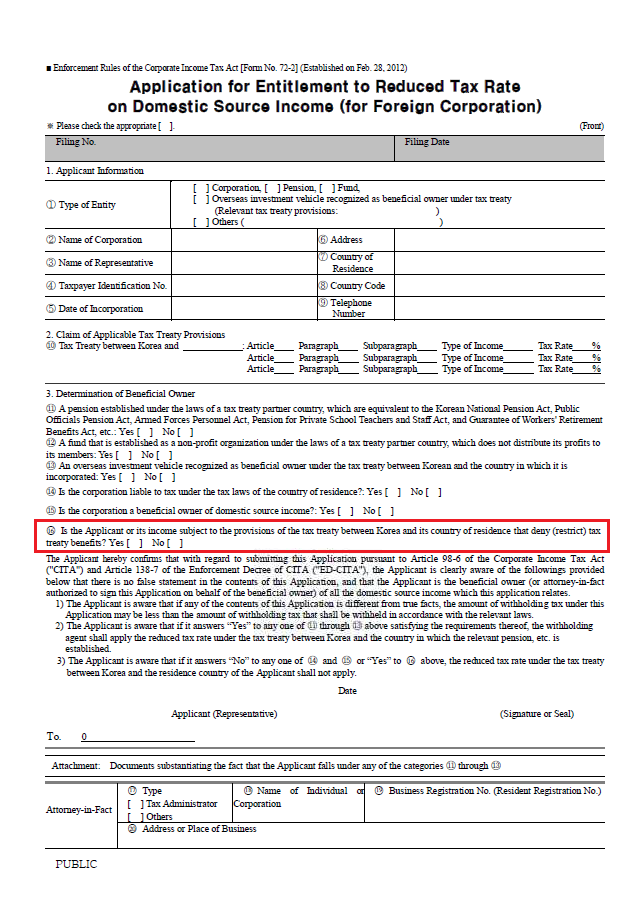

Guide On Completing The Application For Entitlement To Reduced Tax Rate On Domestic Source Income For Foreign Corporation Form No72-2

2

2

Double Taxation Agreement Italy

2

2

2

2

Chapter 8 Are Tax Treaties Worth It For Developing Economies In Corporate Income Taxes Under Pressure

2

2

How To Design A Regional Tax Treaty And Tax Treaty Policy Framework In A Developing Country In Imf How To Notes Volume 2021 Issue 003 2021

2

How To Design A Regional Tax Treaty And Tax Treaty Policy Framework In A Developing Country In Imf How To Notes Volume 2021 Issue 003 2021

Pdf Tax Treaties And The Taxation Of Non-residents Capital Gains

International Taxation

2

International Taxation

International Taxation